Come writers and critics

Who prophesize with your pen

And keep your eyes wide

The chance won’t come again

And don’t speak too soon

For the wheel’s still in spin –Lyrics taken from Bob Dylan’s 1964 classic song, “Times They Are A-Changin’

A look At The S&P 5001

We didn’t have much time to relax and celebrate the S&P 500’s stellar return of 28.7% in 2021. The S&P 500 finished down slightly over 5% in the first month of 2022. This isn’t devastating news as this bellwether U.S. large cap index is similarly only trading approximately 5% below its 52-week high set in late 2021. Clearly, though, this is not the kind of start that warms an investor’s heart. It was only a couple of nice days at January month-end that allowed the S&P 500 to rise back above the 10% loss threshold it had fallen to earlier in the month and that characterizes the minimum decline required for a technical correction. It doesn’t get any cheerier when one conducts some additional slicing and dicing of S&P 500 early stats this year either.

Other equity indexes and stocks

As of Jan. 30, the average S&P 500 stock was trading 16.8% below its 52-week high and roughly one-third of S&P 500 constituents were off more than 20% from their 52-week highs. The largest eight stocks in the S&P 500 that include classic high-growth names, such as Google, Facebook (Meta), Tesla, Nvidia, and Microsoft, are, on average almost 19% off their recent highs. Other major U.S. equity indices fared worse. Both the tech-laden Nasdaq and the small-cap-focused Russell 2000 completed the month down over 9% and ever so close to ending their first 31 days of 2022 in technical correction territory. Riskier areas of the financial markets have suffered far greater pain. Meme stocks such as Game Stop and AMC are close to 80% below their 52-week highs; Bitcoin is off 45% from its highest point in the past 12 months. It hit $69,000 in November 2021 and stands at $37,800 as of this writing.

Risk-averse equity investors

It’s not all that surprising to see this rather modest pullback in large cap U.S. stocks and a more riskaverse attitude in general among equity investors, given not only the strong S&P 500 results in 2021, but the unusually robust 26% compounded annual returns it generated over the last three years…as well as the fact that the S&P had an eerily low maximum drawdown last year of only 6%. In fact, prior to this January, the last time we saw a 10% correction in the S&P 500 was March of 2020. This level of calm is quite abnormal. Since 1957, the inception year of the S&P 500, this index has, on average, experienced one 10% decline as well as more than three 5% declines each year. So, we were spoiled by the level of stability in 2021.

2022: A transition year

It’s way more than just a “the market is due for a rest” phenomenon that is causing this pause and rising volatility in equity land at present, however. 2022 is a transition year for both the market and the economy. A la the classic song that Bob Dylan composed way back in 1964, “Times They Are AChangin’”. There are multiple transitions going on this year:

- Inflation is transitioning from the virtually non-existent levels of 2000-2020 and the historically high figures in 2021 and early 2022, back to what we expect to be more normal historical levels of 3% or so by year-end 2022.

- The Federal Reserve is transitioning from unprecedented accommodation and a “QE forever” mentality from 2008-2021, to less accommodation and a more normal interest rate policy stance this year.

- Fiscal policy is transitioning from massive stimulus, that got us through the COVID-19- inspired economic shutdown in 2020, to more historic norms in government spending this year.

- COVID seems to be in a transition phase from pandemic to endemic as we move through 2022, so some experts believe.

- The economy is moderating from the V-shaped recovery levels of growth in the second half of 2020 and the historically high 5.5% real GDP growth rate we experienced in the United States in 2021, to more normal levels of 2%-3% real growth going forward.

- We will probably see transitions in leadership in Washington this year as well when the mid-term elections are completed in early November.

This is a lot of noise to contemplate, not to mention the additional geopolitical concerns right now, such as potential conflict in the Ukraine, a potential hard landing in the Chinese economy and saberrattling rhetoric regarding nuclear weapon programs in Iran.

“Wall of Worry” items are manageable

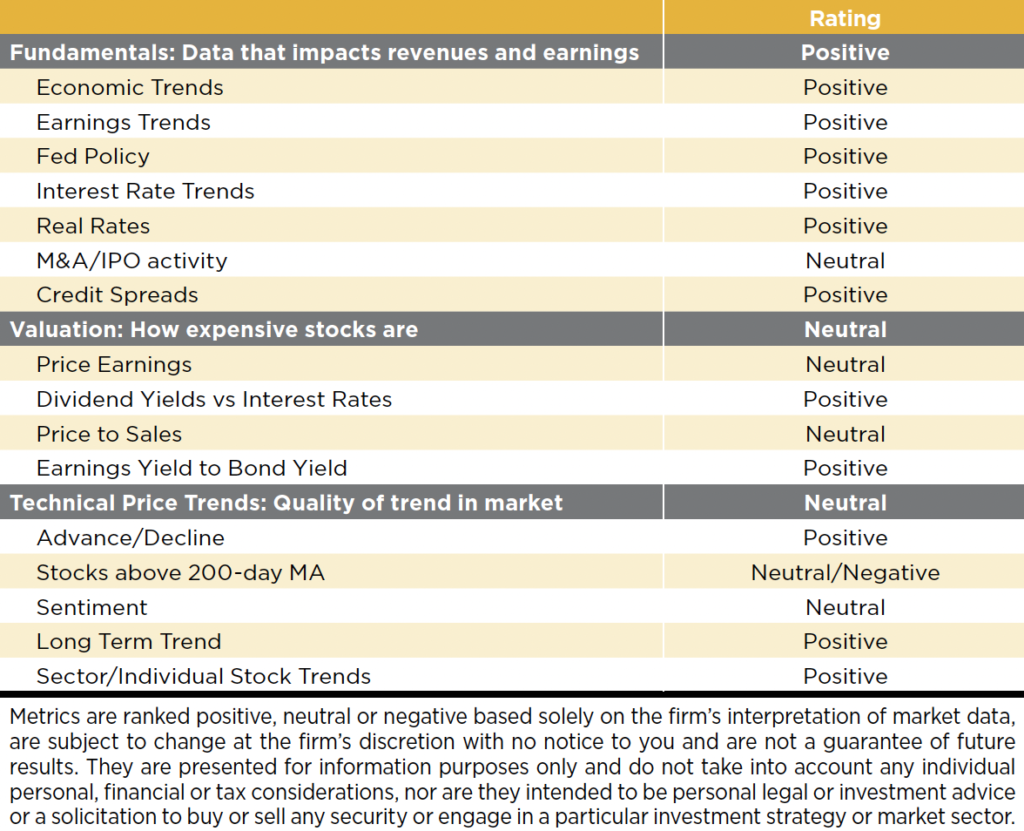

We will address these “Wall of Worry” items and our thought process around them in short order. Suffice it to say that we believe these risks are manageable and that we will avoid feared worst-case outcomes in each case. Additionally, if the facts around these issues deteriorate, they should reveal themselves in the fundamental data we monitor—such as economic growth, earnings growth, interest rate level, and credit spreads. At present, these factors are still positive and healthy. In addition, valuation levels are reasonable in our view, not bubble-like as often advertised, and technical price trends of individual U.S. stocks are still positive when looking at intermediate and long- term charts, not breaking down like we see at prior market tops. This positive fundamental, valuation and technical backdrop is summarized in the chart on the next page.

It is when these three levels of analysis signal warning or negative signs that we become concerned…they are flashing “stay invested” signs to us at present.

Expect a sober market return pace

As we discussed in our Crystal Ball presentation last month, in which we outlined in detail our call for positive returns for US stocks in 2022, we expect the market to advance at a more sober, single-digit return pace this year versus the robust double-digit returns we anticipated and which the market delivered over the last three years. Further, we expect rising volatility due to the comprehensive list of transitional issues cited above, and the uncertainty surrounding them. Despite our belief they will be satisfactorily managed, they are still yet to be resolved. Per Bob Dylan’s lyrics: “Keep your eyes wide…The chance won’t come again…And don’t speak too soon…For the wheel’s still in spin.” The wheel indeed is still spinning, and the patience to stay focused on the facts will be rewarded versus yielding to the fear that can be inspired by headlines during times of transitions. Headlines cause chop, volatility, and yes, temporary corrections that may be significant and in the 15%-20% drawdown range. That said, we would not act on these emotions and fears because corrections are short-lived. It is the fundamental, valuation and technical data that drives markets in the intermediate and long term and they remain healthy.

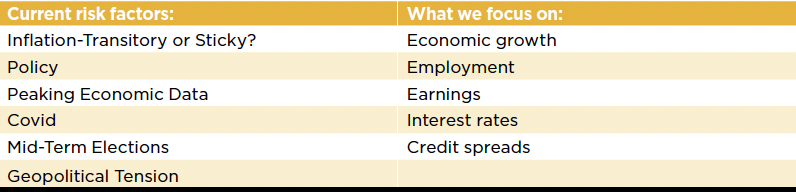

We keep a comprehensive list of current risk items the market faces on an ongoing basis and call this list the “Rolling Wall Of Worry.” Those risk items are listed on the left-hand side of the above table.

They largely center on the transitional issues discussed earlier. As already stated, we believe each risk is manageable but below we discuss our more detailed take on each:

- Accelerating Inflation — Yes, it is robust right now and stickier than usual. Maybe the term “transitional” used last year regarding Fed Chairman Jerome Powell’s opinion of the rise in prices implied too much that it would be very short-lived. But this is semantics. We do not believe it will be sustained at such high levels for a long time. The headline figure of 7% in December is scary, but there are signs of peaking inflationary pressures, such as a respite in transportation prices, comments from key semi-conductor companies that bottlenecks are easing and the same from logistic companies. Further, while the elevated Consumer Price Index (CPI) figures at present are not all related to odd categories, such as used cars and hotel and entertainment price hikes that should be non-recurring, half of the CPI is impacted by these categories, plus energy prices that are unlikely to continue to skyrocket. Once supply chain issues ease further, we believe CPI will as well. We are looking for 3% inflation by year-end.

- Fed Policy Concerns — No doubt, the Fed is taking its foot off the pedal and lightening up on accommodation. We are looking at four or more interest rate hikes this year. But even at this pace, Fed funds should only be at the 2% level by the end of 2023. If inflation is 2%-3% by then, the real Fed funds rate would still be negative and this is still accommodative! In 2000, Fed funds moved up to the 6% level, and real rates are normally a positive 1%-2%. So, the Fed may be hiking but only toward normal.

- Fears of a Peak in Economic Growth — Yes economic growth is slowing but only from robust to normal levels. Slowing from 6%, real GDP growth in 2021 back to a steady eddy 2% to 3% in 2022 and forward is just fine for stocks. There are no major signs of recession at present that generally precede market tops.

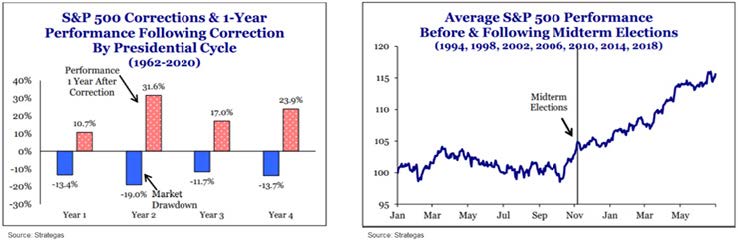

- Midterm Elections — Drawdowns in midterm election years tend to be a bit larger than historical averages because of fears about the potential impact on legislation and policy…somewhere around 19%. In addition, the market tends to trade sideways to down in these years from February to October before rallying at year-end after the election is over and policy fears subside. This is one reason we caution investors to be patient and have low expectations in early Patience should be rewarded by calendar year-end, if the fundamentals remain positive.

- Geopolitical Risks — We continue to monitor what is happening in other parts of the world. But if any portfolio manager tells you he/she has a direct line to Putin, they are lying. One cannot build portfolio strategy around unpredictable shock events like this. What we look for is signs that such fears and events are spilling over into the fundamentals, such as causing a slowdown in specific economic activity, e.g., trade activity, or that they are driving a rise in energy prices that can stall an economy, etc.

Wrap-Up

Given our general view of positive but more sober equity returns in 2022, our expectations for rising volatility associated with higher risk levels in a transition year, and our belief that a significant shortlived correction is highly probable this year, what do we recommend investors do this year:

- Make sure you talk to your wealth advisor about the benefits of rebalancing back to your long-term strategic asset allocation if the robust returns of the last three years have caused your stock allocation to rise well above your long-term strategic target.

- Steel up for a potential significant, but brief, correction. Don’t freak out. Remain patient given the still positive fundamental, valuation and technical backdrop. This will help investors avoid the whiplash and regret of selling too soon…think of 2020. The 34% swoon in March 2020 was quickly followed by a 90%-plus advance during the balance of the year. In addition, if you have already rebalanced back to your long-term strategic target, this should provide the courage to add to your equity exposure following a pull-back at attractive entry points.

- Maintain balance in your U.S. large cap positioning and a blend of both growth and value holdings as we see swift rotation in leadership from one camp to another time and again in this more volatile environment. Consider embracing international and small-cap equity exposure if you are light in allocations in these areas.

Our view would be much more cautious and defensive if things change dramatically and we begin to expect more ] troublesome inflation and some kind of surge in interest rates. That is not our base case or a high probability event in our view at present. For now…Stay the Course!

Sources

1 Factset data

The S&P 500 Index is a market-value weighted index provided by Standard & Poor’s and is comprised of 500 companies chosen for market size and industry group representation.

The Russell 2000 index is an index measuring the performance of approximately 2,000 smallest-cap American companies in the Russell 3000 Index.

The Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange.

The impact of COVID-19, and other infectious illness outbreaks that may arise in the future, could adversely affect the economies of many nations or the entire global economy, individual issuers and capital markets in ways that cannot necessarily be foreseen. The duration of the COVID-19 outbreak and its effects cannot be determined with certainty.

Asset allocation is a strategy designed to manage risk but it cannot ensure a profit or protect against loss in a declining market.

This commentary is limited to the dissemination of general information pertaining to Mariner Platform Solutions’ investment advisory services and general economic market conditions. The views expressed are for commentary purposes only and do not take into account any individual personal, financial, or tax considerations. As such, the information contained herein is not intended to be personal legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. Nothing herein should be relied upon as such, and there is no guarantee that any claims made will come to pass. Any opinions and forecasts contained herein are based on information and sources of information deemed to be reliable, but Mariner Platform Solutions does not warrant the accuracy of the information that this opinion and forecast is based upon. You should note that the materials are provided “as is” without any express or implied warranties. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. Past performance does not guarantee future results. Consult your financial professional before making any investment decision.

Investment advisory services provided through Mariner Platform Solutions, LLC (“MPS”). MPS is an investment adviser registered with the SEC, headquartered in Overland Park, Kansas. Registration of an investment advisor does not imply a certain level of skill or training. MPS is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which MPS transacts business and maintains clients. MPS is either notice filed or qualifies for an exemption or exclusion from notice filing requirements in those states. Any subsequent, direct communication by MPS with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about MPS, including fees and services, please contact MPS or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you invest or send money.

Investment Adviser Representatives (“IARs”) are independent contractors of MPS and generally maintain or affiliate with a separate business entity through which they market their services. The separate business entity is not owned, controlled by or affiliated with MPS and is not registered with the SEC. Please refer to the disclosure statement of MPS for additional information.